Ruskin Felix Consultancy is an incubator for Watertilt, a leading aquatech company that focuses on water as a resource and builds businesses for water sustainability, conservation, and technology. Watertilt aims to create a global water network that connects water users, providers, and innovators. It offers various solutions, such as water quality monitoring, water trading, water optimization, and water education. It is also developing a blockchain-based platform that will enable transparent and secure transactions of water rights and credits.

We support Watertilt’s growth by providing expert advice on business strategy, financial management, and risk mitigation. Ruskin Felix Consultancy also conducts market research and feasibility studies for new products and services, develops business plans and financial models for fundraising and scaling up, evaluates the environmental, social, and economic impacts of Watertilt’s solutions, and facilitates partnerships and collaborations with other stakeholders in the water sector. By supporting Watertilt, we are contributing to the improvement of water quality and safety, the reduction of water wastage and inefficiency, the enhancement of water security and resilience, the increase of access to clean and affordable water, the promotion of water awareness and education, and the support of water governance and cooperation. These are some of the benefits that Watertilt’s solutions can bring to the environment and society.

Ruskin Felix Consulting is committed to giving back to society by supporting Watertilt, we hope to make a positive difference in the world’s water resources. By working together, we aim to address some of the most pressing challenges of our time, such as water scarcity, pollution, climate change, and social inequality.

In our shared vision for a sustainable future, RFC with Watertilt are trying to continuously push the boundaries of innovation. We aspire to enrich knowledge to different communities, industries and governments about water management in order to safeguard our future.

Ruskin Felix Consulting (RFC) collaborated with Regence Inc. to address technology risks and create a comprehensive Training & Development Strategy for Salesforce, considering the challenges posed by the COVID-19 pandemic. As the industry and competitors faced disruptions due to the pandemic, RFC worked closely with Regence Inc. to implement a transformative workforce strategy, giving them a significant competitive advantage and enabling them to gain a larger market share.

The overall strategic plan devised by RFC spanned one year and focused on creating Strata-based learning and development levels, promoting a mindset shift, and fostering an inclusive integrated structure aligned with organizational goals. The plan comprised three key components:

Training & Upskilling Program: RFC designed a comprehensive training and upskilling program to equip the salesforce with the necessary skills and knowledge to adapt to the changing market landscape. This program ensured that the workforce remained competent and competitive in the digital era.

Leadership Development Program: To strengthen leadership capabilities, RFC formulated a leadership development program that honed the skills of existing leaders and identified emerging leaders within the organization. This program aimed to cultivate a pool of competent leaders capable of steering the company towards success.

Actualization Program: The actualization program provided employees with the resources and support they needed to actualize their potential, fostering a positive work environment and enhancing employee engagement.

Additionally, RFC assisted in developing core sales development policies and a transformational development policy. These policies were strategically designed to optimize the use of data and resources, increase sales conversion rates, and boost overall productivity.

In line with the new digital, work-from-anywhere environment, RFC helped Regence Inc. innovate and invest in new products to cater to changing customer needs and market demands. This strategic investment bolstered the company’s competitive edge and positioned them to capitalize on emerging opportunities.

By partnering with RFC, Regence Inc. successfully navigated technology risks and embraced a forward-thinking Training & Development Strategy that empowered its workforce, driving business growth, and establishing a dominant presence in the market.

While working for the roofing contractor’s industry, which is a large and growing market that is expected to reach USD 51.9 billion in 2021. We have provided comprehensive market research, competitive analysis, pricing strategy, traffic analysis, key competitive advantages, and customer acquisition strategies for the industry. These documents and analyses provide valuable information and insights on the current and future trends, challenges, opportunities, risks, and strategies in the industry.

The roofing contractors’ industry is driven by factors such as the increasing demand for roof replacements and repairs, the rising adoption of energy-efficient and eco-friendly roofing materials, the growing construction activity in residential and commercial sectors, and the favorable government policies and initiatives for green buildings.

The industry is also facing challenges such as low barriers to entry, high competition, labor shortages, weather uncertainties, and fluctuating raw material prices. The industry is segmented by service (roof installation, roof maintenance and repair), product (asphalt shingles, metal roofing, single ply roofing, coatings, low slope asphalt), end user (residential, commercial), and geography.

We have analysed the pricing strategies of different competitors in the roofing contractors’ industry, based on their service features, target segments, value proposition, cost structure, and competitive advantage. We have also provided a comparison table of the pricing plans and features of each competitor. We have suggested some best practices and tips for setting a pricing strategy that can maximize revenue and customer satisfaction.

We have also provided a traffic analysis dashboard that shows the traffic volume, quality, conversion rate, bounce rate, average session duration, and other key performance indicators for each competitor. We have also provided some recommendations for improving traffic generation and optimization. We have identified and highlighted the key competitive advantages of each competitor in the roofing contractors’ industry, based on their service differentiation, innovation, customer service, brand reputation, market presence, partnerships, and awards. We have also provided some examples of how each competitor leverages their competitive advantage to attract and retain customers.

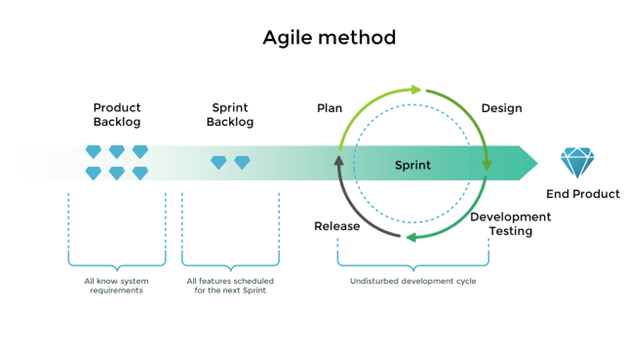

In today’s dynamic business environment, adapting to change and finding ways to innovate quickly is a must for staying competitive. RFC helps in decoding agile consulting by providing the agile methodology that enables your organization to achieve this and more with unparalleled speed, quality and reliability.

However, implementing the cultural shift towards agility can be challenging for businesses. Suppose you find yourself struggling to adopt an Agile approach or want to optimize your current processes further. In that case, partnering with experienced agile consultants can be advantageous in driving your Agile transformation forward while maximizing its benefits. In this article, we will be discussing in detail what is agile in project management and why it is important for businesses to adopt agile.

WHAT IS AGILE PROJECT MANAGEMENT?

Agile is an innovative project management approach frequently used in software development which involves delivering working software frequently to clients or end-users by breaking a project down into 1-4 week iterations called “sprints“.

Emphasizing collaboration and transparency, agile methodology ensures developers and stakeholders work closely to ensure everyone is aware of the project’s progress while creating quick responses to changes in requirements. Agile practices are important for large-scale projects with unclear outcomes prone to rapid change.

DEFINING AGILE CONSULTING

Agile consulting is an approach that helps organizations embrace agile methodology to optimize their product development, project management and even organizational culture. The approach is context-specific, tailored to the client’s unique needs and requirements. Agile consulting incorporates the principles and values of agile methodology that emphasize collaboration, flexibility and rapid response to changes. However, it also considers restrictions within the organization to avoid any possible hindrances in adopting agility at large.

ADOPTING AGILE CONSULTING

Many organizations are adopting Agile due to only one reason which is Flexibility.

The Agile methodology is a dynamic approach aimed at increasing business flexibility and adaptability in ever-changing environments. The technique breaks down larger projects into more manageable portions enabling quick delivery of results (usually two weeks or less). Thus, allowing organizations to pivot quickly in response to changes driven by evolving customer needs to be fostered by flexible adaptation solutions.

The pros and cons of agile consulting for a business are as follows:

BENEFITS OF AGILE CONSULTANCY

Improved efficiency

Partnering with an Agile consultant can save you considerable time and resources in implementing Agile frameworks. Leveraging the expertise of specialized consultants in adopting agile methodologies ensures organizations avoid common mistakes and delays that may arise in the process.

Flexibility

Agile consultants are very flexible in how they work, meaning they can easily adapt to your organization’s unique needs and culture.

Outside Perspective

When it comes to assessing internal processes objectively and identifying areas of improvement, organizations often face difficulties. Agile consultants can help bring a fresh external perspective that facilitates this task while bringing value to the organization by offering innovative solutions and ideas not previously considered.

Expertise and experience

Agile consultants possess broad exposure to agile methodologies within several industries and are well-positioned to understand how to apply them practically. They’ve specialized processes providing innovative solutions while utilizing their experience to avoid common pitfalls ensuring the successful implementation of agile methodology into your organization.

ROLE OF AN AGILE CONSULTANT

Implement agile frameworks to best fit a client’s specific requirements

Develop a detailed process backlog and roadmap

Adapt swiftly to change and feedback throughout each development cycle

Conduct interviews to identify inefficiencies in an organization’s current processes that need improvement

Leverage approaches and methods based on the science of memory retention

Promoting collaboration and communication across different teams and departments

Expertise in fundamental concepts such as Agile principles, Lean thinking frameworks (Kanban) and software development life cycle procedures (SDLC)

AGILE COACH VS AGILE CONSULTANT

An agile coach is committed to helping individuals and groups in an organization adopt the Agile framework providing continuous education and support. They typically work on a long-term basis with teams providing guidance for successful outcomes.

In contrast, an agile consultant is more dedicated to facilitating a company-wide transformation towards Agile methodology. This includes undertaking tailored organizational planning, implementing related processes and tools and providing comprehensive educational training sessions at all levels of a firm.

While both roles are important in helping organizations successfully adopt Agile methods, the decision of whether to work with an Agile consultant or an Agile coach (or both) will ultimately come down to your specific goals.

WHEN SHOULD YOU HIRE AN AGILE CONSULTANT?

In today’s fast-paced business world, delivering true value requires efficient, faster and less expensive solutions. Adopting Agile methodologies is incredibly beneficial as it ensures businesses keep up with the ever-changing landscape.

Agile consultants offer extensive experience in a variety of projects, frameworks and industries making them well-versed in fueling the adoption process with tailored planning and facilitating effective implementation of best practices. They continuously build on their expertise through relevant certifications in software and processes and train teams effectively for optimal productivity.

Businesses can also rely on Agile consultants when having trouble gaining a full perspective on what works best within providing effective solutions that meet company needs using structured approaches tailored towards organization-specific processes.

CONCLUSION

At Ruskin Felix Consulting LLC, we strongly believe that our range of Agile consulting services has proven time and time again to be a game-changer in the consulting industry. We are up to date on the latest methodology trends to keep your business competitive and move your organization forward. Our personalized approach ensures that we always act with your best interests at heart; delivering tailor-made solutions unique to each client’s needs to guarantee ultimate satisfaction.

Ruskin Felix Consulting LLC can be your expert consultative partner with vast experience and flexibility in deploying the most modern technologies for phenomenal results. We embrace ‘Agile’ as our core value and approach to deliver solutions that meet your needs. Please feel free to contact us at contact@ruskinfelix.com for more information.

A strong business plan is crucial for the growth and success of any enterprise. It serves as a roadmap for entrepreneurs, providing a clear vision of the company’s goals, strategies, and tactics.

A good business plan helps in identifying potential customers and exploring competitive advantages. It also serves as a tool for seeking financing, persuading investors, and securing funding. In today’s fast-paced business environment, having a well-crafted business plan can give a company a competitive edge.

By outlining financial forecasts, income statements, and balance sheets, a business plan provides insight into the financial information necessary for making informed decisions. A lean startup plan can help a business avoid unnecessary expenses and optimize the production process. Using industry-specific templates can also streamline the planning process, making it more efficient and effective.

With a good business plan in place, entrepreneurs can confidently navigate the foreseeable future, while keeping an eye on customer segments and staying ahead of the competition. In this article, we will explore the key components of a strong business plan and how it can help businesses achieve sustainable growth.

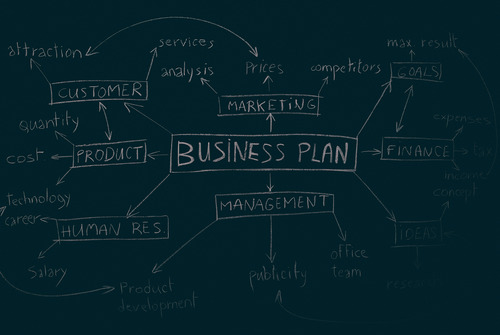

CONCEPTS INCLUDED IN DEVELOPING TRADITIONAL BUSINESS PLANS

A business plan serves to describe the business structure of the proposed venture in order to exploit a concept. Traditionally, there are three main functions of a business plan:

Action Plan

Writing a business plan or creating a new business plan template can help you to move forward in taking action towards developing a full-proof marketing plan and strategy for establishing the business concept or engaging in a new venture.

Starting a small business or any business for that matter may seem daunting, but breaking down the process into smaller tasks and allocating these tasks to the management team can make it less intimidating. By solving smaller problems, you can eventually solve larger problems.

Road Map

Once your business plan has been executed and is now an established business, this business plan would serve as a valuable tool to keep you on track and moving towards your long term objectives and goals.

Business planning also requires working within the revenue and expense projections and keeping financial statements in check.

Changing an existing business plan

In the midst of developing a formal business plan, it is easy to lose sight of the bigger picture, but a business plan can help keep you focused on your objectives.

In addition, it can help others, such as suppliers, customers, employees, friends, and family, understand your target market and vision.

Sales Tool

A well-written business plan can also serve as a sales tool. You will likely need financing from investors to start your business and a business plan is essential in convincing them to invest in your venture.

It can also help you negotiate concessions from suppliers or customers. Finally, a business plan can help you convince family members and even yourself of the potential benefits of proceeding with your concept.

HOW TO WRITE A BUSINESS PLAN

To prepare a business plan that is effective for any audience, it is important to follow some basic guidelines.

These guidelines should cover the essential elements of the plan. Here are the guidelines:

Company description:

The company and business plan format should be straightforward. The one- or two-page introduction statement is crucial. To make the strategy easy to understand, utilize basic language.

Key elements for market analysis:

The market is more critical than the product. Investors and consumers are interested in how the market will receive the products and services, so you need to provide evidence that shows how your products and services meet their needs.

Business idea for a clear distribution strategy:

Companies need a business plan for making up an efficient distribution strategy. The business plan templates should outline a clear strategy that will enable you to distribute your goods and services effectively. You should describe the methods, costs, logistics, warehousing and delivery arrangements that will be used.

Market research for having a competitive edge:

You need to show what will make your business unique and different. For example, you might mention special attributes such intellectual property such as patents, copyrights or strategic partnerships that give you a competitive edge.

Business plan software:

You should highlight the strength of your management team in terms of their experience, qualifications and achievements. You should also explain how the policies you have put in place will help to attract investors and retain key employees.

Realistic projections based on cash flow statement:

Your projections for the future must be credible, realistic and substantiated with valid assumptions.

Focus on the end user:

Remember who your audience is. Bankers and financiers want to see stability, security, cash flow coverage and good returns, whereas venture capitalists are more interested in high leverage with correspondingly high returns.

Your business plan should reflect this by showing how funds invested are secured and how cash flows will more than cover interest and principal payments.

THE STRUCTURE OF A BUSINESS PLAN

When it comes to starting a new business or expanding an existing one, having a solid business plan is essential.

A business plan outlines your goals and objectives, identifies potential challenges, and provides a roadmap for achieving success.

But what are the key elements that make up a successful business plan? Let’s take a closer look at the structure of a typical small business owner’s plan.

Executive Summary:

The executive summary is a brief overview of the entire business plan. This section should provide a snapshot of your business idea, highlighting the key features traditional business plan that make it unique and demonstrating its potential for success.

Make sure you have a strong business plan template:

The company description provides an overview of your business, including its history, mission, and vision. This section should also provide information on your business loan target market, competitors, and industry trends.

Take the help of financial institutions and conduct Market Analysis:

The market analysis section should demonstrate a clear understanding of the industry and market you plan to operate in. This includes information on your target market, customer needs, and market trends.

Products or Services:

This section should describe your products or services in detail, highlighting their unique features and benefits. It should also provide information on how you plan to produce or deliver them.

Marketing and Sales:

In this section, you’ll describe your marketing and sales strategies, including how you plan to reach your target audience, promote your products or services, and generate revenue.

Operations and Management:

This section should outline your operational plan and business intends, including how you plan to manage the day-to-day operations of your business. It should also provide information on your management team and their qualifications.

Financial Plan:

The financial plan is perhaps the most important section of your business plan. It should include financial projections, such as income statements, cash flow statements, and balance sheets, as well as information on funding requirements and how you plan to use any funds raised.

HOW A BUSINESS PLAN OUTLINE SHOULD BE LIKE

Running a successful business can be super tough. There are tons of responsibilities to juggle, and it’s easy to get side tracked. However, with a strong business plan in place, you’re more likely to achieve sustainable growth.

Sure, it’s not the most exciting aspect of launching or running a business. But creating a comprehensive plan upfront can save you heaps in time and resources down the line.

But how do you create a great business plan? Let us shed some light on that.

First off, make sure to include your brand’s story and voice throughout your roadmap. It needs to embody your brand’s message from top to bottom. Too often entrepreneurs only focus on revenue projections and basic goals but miss out on telling the story that drives those aspirations.

Another important factor when doing business finances and drafting up an excellent business plan is budgeting accurately – I learned this one the hard way! Being able to show where every dollar goes is vital when fighting for investor capital or loans from financial institutions.

Moreover, don’t just talk about today; think about where your brand could go tomorrow! Planning far into the future through forecasting models shows potential investors that there is true longevity attached instead of saying “We’ll figure it out later.”

Incorporating several literary devices such as rhetorical questions and metaphors also makes writing compelling and engaging for readers.

Anecdotes can also add some flavor into any post – like this time I tried selling my lemonade stand for $1 million dollars because Starbucks had bought coffee machines at that price point HA-HA (that didn’t work out too well).

All jokes aside – developing an in-depth strategy should never be taken lightly but instead cherished as an opportunity to reinforce existing branding and marketing strategies while carving out new spaces for growth.

So if everyone aims for steady growth in your biz, take time beforehand crafting solid business plans, that reflect your mission statement and brand standards while incorporating data-backed research at each step along the way- seriously!

CONCLUSION

A strong business plan is critical for achieving sustainable growth in any business. It not only provides a roadmap for achieving short-term goals but also sets the foundation for long-term success.

Through careful research and analysis of industry trends and consumer behavior, entrepreneurs can identify new market opportunities that they can capitalize on.

By including the brand’s story and voice throughout the roadmap, a business plan can embody the brand’s message from top to bottom. Accurate budgeting, forecasting models, and data-backed research are also essential components of a comprehensive business plan.

Additionally, incorporating literary devices such as rhetorical questions and anecdotes can make the writing more compelling and engaging for readers.

But a business plan is more than just a document – it’s a living, breathing strategy that needs to be revisited and updated regularly.

As market conditions change and consumer needs evolve, entrepreneurs need to adapt their plans accordingly. This requires a willingness to be flexible and a commitment to continuous learning and improvement.

At Ruskin Felix Consulting, we help businesses to devise an optimal business plan for established businesses and established companies to ensure that their business grows whilst maintaining their financial health.

Lean management is a way of running a business that aims to improve quality and efficiency by getting rid of unnecessary resources like time, money and effort. It can also be called lean production or lean manufacturing. The goal is to deliver only the best and most useful services or products for customers and clients at the right cost.

Lean management started in the Japanese manufacturing industry in the 1990s with the Toyota Production System (TPS). Toyota was a small automaker that became successful worldwide, so it’s business and operational process became popular. Other companies soon followed similar methods hoping to get the same level of success. Now the lean management concept is widely used by top businesses around the world such as Intel, John Deere and Nike.

Benefits of lean management

A Decrease in Cost

Lean management is about increasing profits. The selling price is affected by various factors that may depend on product qualities or actual demand in markets but usually, companies can control their costs better and lean practices help to reduce costs so that all savings can go to profit.

Improved Customer Interactions

Lean management started with the customer’s perspective in mind. The way they talk to staff, how their issues are solved and their experience with the product are some of the main reasons for eliminating wasteful practices. If customer surveys are showing a certain trend then leaders should notice what the company can lose. As a result customer interactions and overall service should get better.

Utilization of “Push and Pull”

Company costs can increase if leaders are not watching how inventory is stacking up. A strategy that can help with this is having a “pull” instead of a “push” mentality. This means that earlier production stages depend on what is happening in later processes. This can help companies avoid the problem of making too much and paying a higher holding cost. Companies will only order what they need.

Increased Quality

Lean management is also about paying a lot of attention to details. The goal is to reduce the number of errors and fixes in products. This action means that processes will be improved to prevent mistakes which saves time that workers will have to spend to redo products and the money needed to pay them for the work.

When a company realizes the value of lean management and starts to apply the strategies then a new way of thinking begins to emerge in the company. Workers are more willing to improve and are looking for ways to constantly make the work they do even more effective. Introducing teams to lean management can create a culture that values continuous workflow and daily improvement.

Increased Employee Morale

Since the principles of lean management supports an approach where managers are in frequent communication with employees about their work and their process, employees could feel they have more control over their decisions. Workers know where they stand and their areas of improvement to produce quality work.

What are lean principles?

Lean management principles are aimed at creating a stable workflow that maximizes the company’s performance while minimizing waste. This approach is becoming increasingly popular as consumer demands continue to evolve and companies look for ways to improve their work processes.

Lean management is based on these main lean principles. The five principles of lean are defining customer value, mapping stream value, creating flow, setting up pull and seeking perfection.

Defining Value

This principle determines the value of a product or service from the customer’s point of view. Rotating Solutions emphasizes the importance of making and focusing on a timeline for the production process including delivery. This can include outlining key requirements, price points, expectations and other vital information.

Mapping Stream Value

This principle is also called waste mapping. It looks at all steps of any given business process to find out which unneeded actions and resources can be removed to increase efficiency.

Create Flow

This principle concentrates on achieving efficiency and speed as well as making sure that multiple operational tasks are done as fast and smoothly as possible to achieve maximum efficiency without compromising quality.

Establishing Pull

Make a flow in which there are only enough materials and resources to produce the needed products on time and in a steady way.

Pursuing Perfection

Basically, this last lean principle means ensuring that the other four principles happen constantly and regularly. Make sure all employees are also aligned with the final lean goal.

Implementing a lean management system

Conducting a current state analysis

To start using the principles of lean management you need to assess the current situation and find out what needs to change. You do this by looking at how things work now finding out where the problems are and figuring out why they happen. This helps you spot waste and opportunities for improvement such as making processes simpler, faster or better. You can use tools like value stream mapping, process flow analysis and waste analysis to do this assessment.

Establishing a clear vision and goals

Once you have assessed the current situation, you need to set a clear vision and goals for the lean management system. This means deciding what you want to achieve with the lean system, what the scope and limits are and how you will get there. A clear vision and goals guide the implementation process and help make sure that everyone in the organization is on the same page and working for the same outcomes. You should also set key performance indicators (KPIs) to track progress and success against the goals. A well-defined vision and goals help organizations to focus their efforts and keep improving continuously.

Leadership support is essential for effective lean implementation. Leaders must lead the lean initiative and explain its value to the organization. They must also allocate resources and eliminate any obstacles to lean thinking and implementation.

Resistance to change

People usually don’t like change, especially if it means changing established processes and procedures. It is important to include all stakeholders in the implementation process and explain the advantages of the lean methodology to get support and lower resistance.

Inadequate training

Lean involves a big change in how work is done, and employees need to be properly trained to adjust to the new processes. Offering thorough training and ongoing learning opportunities can help employees cope with the changes and ensure effective implementation of lean production system.

Lack of standardization

Making processes and procedures consistent is a key part of lean implementation. Standardization helps to spot waste and inefficiencies and makes it easier to implement continuous improvement initiatives. It is important to set clear rules and procedures and ensure that everyone follows them.

Insufficient metrics and feedback mechanisms

To measure progress and make decisions based on data it is important to set metrics and feedback mechanisms. It is essential to monitor performance, find areas for improvement and communicate progress to stakeholders.

Continuous improvement with lean management

Continuous improvement using Lean principles makes things better for students, faculty, staff and other customers. It also involves the people who do the work in improving the work, resulting in more time spent on interesting work, more balanced workloads, less crisis management and less stress. Moreover it creates value for the organization through significant improvements in the areas of financial, operational delivery, quality and experience and engagement.

Lean is also about creating a culture that values all employees and allows them to look for ways to improve their work and share ideas for continuous improvement. It is a systematic deliberate model for making and maintaining an environment where continuous improvement is the norm.

Conclusion

To implement lean management principles successfully it is important to start with a clear understanding of the current state of your organization’s processes and identify areas that could benefit from improvement. You should also involve your employees in the process and provide them with the training and support they need to implement the changes.

We at Ruskin Felix Consulting help clients generate long-term value for all stakeholders. We help clients transform, grow and operate while fostering trust through assurance with our services and solutions. Please feel free to contact us at contact@ruskinfelix.com

A business growth strategy is a plan developed by an organization to achieve its objectives and expand its operations. A successful growth strategy requires a thorough assessment of the current state of the business, identification of opportunities for growth, setting realistic and measurable goals and implementation of the right strategies. This article outlines the steps to developing a successful business growth strategy.

Importance of Developing a Successful Business Growth Strategy

Developing a successful business growth strategy is essential for the survival and growth of any organization. Through a successful business growth strategy businesses can:

Increase market share and revenue.

Expand into new markets and geographical locations.

Build brand equity and customer loyalty.

Develop new products or services to meet changing customer needs.

Diversify their offerings and minimize risks.

Create opportunities for innovation and differentiation.

Assessing the current state of your business

Identifying SWOT

Before developing a growth strategy, it’s essential to assess the current state of your business which can be achieved by conducting a SWOT analysis i.e., strengths, weaknesses, opportunities and threats. A SWOT analysis provides an overview of the business’s internal and external environment. It helps you assess internal factors that might affect your business (strengths and weaknesses) and external factors (opportunities and threats).

Conducting Market Research

Market research is a critical aspect of developing a growth strategy which involves gathering information about the industry, target market and customers’ needs and preferences. This information can be used to identify market trends, customer behavior and preferences which can be leveraged to develop products or services that meet their needs.

Analyzing Competitors

Competitor analysis includes gathering information about your competitors’ strengths, weaknesses, opportunities and threats which can be used to identify competitive advantages and gaps in the market that can be exploited to gain a competitive edge. Analyzing the strategies of one’s competitors can be used offensively and defensively to better spot opportunities and threats.

After assessing the current state of your business and conducting market research one must set realistic and measurable goals for the organization. These goals should be specific, measurable, achievable, relevant and time-based (SMART) which should be aligned with the organization’s mission and vision. Defining these parameters as they pertain to your goal helps in ensuring that your objectives are achievable within a certain time frame.

Defining Objectives for Business Growth

Defining objectives for business growth involves identifying specific outcomes that the organization seeks to achieve. These objectives must be well-defined, clear and aligned with the overall business strategy. When you develop a list of business objectives you must focus on the specifics which means analyzing, assessing and understanding where you are now and where you want to be in the future. The objectives must be challenging but also achievable for the team.

Creating Key Performance Indicators

Once the objectives have been defined the next step is to create key performance indicators. KPIs are a set of quantifiable metrics used to track progress toward achieving objectives. They help businesses understand how well they are performing and whether they are on track to meet their goals. KPIs can be financial or non-financial and should be specific, measurable and relevant to the objective.

Establishing a Timeline for Achieving Goals

Establishing a timeline for achieving the goals is essential which helps to keep everyone accountable and ensure that progress is being made toward achieving the objectives. It is important to set deadlines for each objective and to break down the objectives into smaller and achievable tasks that help in ensuring that the objectives are being met on time.

To sum it up it is essential for each organization to establish objectives that are both attainable and quantifiable. To succeed in a company, it is crucial to define growth objectives, develop KPIs and set a deadline for accomplishing targets. Setting and monitoring specific goals allows firms to pinpoint where they need to make changes to finally succeed.

Identifying growth strategies

Identifying growth strategies is crucial for businesses looking to expand their operations, increase market share and improve profitability. There are several growth strategies available and businesses need to choose the one that suits their goals, capabilities and resources.

Here are some of the key business growth strategies and how they can be implemented:

Market Penetration strategy

Market penetration involves increasing existing product or service sales in the current market. Companies can achieve market penetration by adopting various tactics such as lowering prices, improving product quality, increasing advertising and promotions and enhancing customer service.

Market Development

Market Development strategy involves introducing existing products or services into new markets. Companies can achieve market development by targeting new geographical locations, customer segments or distribution channels.

Product Development growth strategy

This growth strategy involves creating new products or services to cater to existing markets. By investing in research and development, acquiring new technologies or leveraging existing capabilities companies can develop their product.

Diversification growth strategy

Diversification involves expanding into new products and new markets simultaneously. Companies can diversify by acquiring other businesses, launching new product lines or entering new markets through strategic partnerships.

Each growth strategy has advantages and disadvantages and businesses must carefully evaluate their options before deciding on the best approach. By identifying and implementing an appropriate growth strategy companies can position themselves for sustained growth and success in the long run.

This strategy focuses on growing the business using internal resources such as increasing efficiency or productivity, expanding existing products or services and improving customer retention. Organic growth aims to achieve sustainable growth over time without relying on external resources or acquisitions.

Marketing Strategy

An effective marketing strategy is essential for achieving business growth i.e. identifying target demographics, developing campaigns that resonate with them and identifying the most effective channels for reaching them. Key metrics to track include customer acquisition costs, customer retention rates and annual sales growth.

Customer Retention

Retaining existing customers is critical for achieving business growth which involves identifying and addressing the needs of existing customers, developing loyalty programs and improving customer service. Key metrics such as customer retention rates, customer lifetime value and customer satisfaction should be tracked.

Market Segmentation

Segmenting the market based on customer needs and preferences can help businesses target their messaging and offerings more effectively. By dividing the sample size into smaller groups on the basis of gender, age, buyer personas and other segments companies can market their products effeciently.

Implementing the growth strategies

Implementing growth strategies is essential for businesses to expand and achieve long-term success. To effectively implement growth strategies companies need to follow a well-structured approach that includes identifying and allocating resources, creating a plan of action and establishing a monitoring and evaluation system.

Identifying and Allocating Resources

The first step in implementing growth strategies is identifying the necessary resources required for the growth plan. This includes identifying the financial, human and material resources required to execute the plan effectively. Once the resources are identified companies need to allocate them effectively to ensure that they are being utilized optimally.

Creating a Plan of Action

Once the necessary resources are identified and allocated the next step is to create a plan of action. The growth plan should outline specific goals, objectives and timelines that are realistic and achievable. The plan should also identify potential risks and challenges and outline strategies to overcome them. It is important to involve all stakeholders in the planning process to ensure that everyone is on the same page.

Establishing a Monitoring and Evaluation System

To ensure that the growth plan is being executed effectively companies need to establish a monitoring and evaluation system that involves setting up key performance indicators (KPIs) to measure progress and identify areas that require improvement. Regular monitoring and evaluation of the growth plan will help companies stay on track and make necessary adjustments to the plan if required.

Measuring and Evaluating the Success of the Growth Strategy

Measuring and evaluating the success of the growth strategy is essential to determine whether the business is achieving its objectives. The first step in measuring and evaluating the success of the growth strategy is to establish key performance indicators (KPIs) that align with the business’s objectives.

The next step is to regularly monitor and evaluate the KPIs. Monitoring should be done at regular intervals, such as monthly, quarterly or annually. The evaluation process should involve a comparison of the actual results with the set targets. The evaluation process should identify any areas where the business is falling short of the set targets and provide recommendations on how to improve.

Analyzing the Effectiveness of the Growth Strategies

Analyzing the effectiveness of the growth strategies involves examining the outcomes of the strategies to determine whether they are achieving the desired results. The analysis should involve examining the various aspects of the growth strategies i.e., marketing, sales, operations and customer service. The analysis should identify the areas where the strategies are most effective and those where improvements are needed.

Adjusting the Growth Strategy

Based on the results of the analysis adjustments should be made to the growth strategy. The adjustments should be based on the areas where the growth strategies are most effective and those where improvements are needed. It may include changes in marketing strategies, sales approaches, customer service or operational procedures.

Celebrating Success

Celebrating success is an important component of a successful business growth strategy. Recognizing the achievements of the business and the people who contributed to those achievements helps in motivating employees, creating a positive culture and attracting new customers.

Examples of Successful Business Growth Strategies

Facebook

A good example of a brand that succeeded using market penetration is Facebook. When they started out they were accessible only to Harvard University students. After that, they expanded their accessibility to Stanford, Yale and Columbia. Eventually, they were available to all Ivy League and several schools and then all colleges in the U.S. and Canada. Later they spread to audiences beyond college-going students.

Slack

The e-communication platform gained attention by replacing the traditional email system with a more convenient platform for the working community.

Dollar Shave Club

Venture into new markets is another successful business growth strategy employed by many brands that became successful. In 2012, Dollar Shave Club a male razor manufacturer entered the retail marketing model dominated by a direct-to-consumer strategy offering a cheaper alternative to the market leader. The new expansion plan for Dollar Shave Club cut out the middlemen and gave savings to the customers. This dissolved Gillette’s market to about 53% in 2019. Five years later, Unilever acquired Dollar Shave Club for $1 billion.

Google

Google aced it by successfully integrating AdWords into its B2C product flow. It was able to keep its search engine speed by including text advertisements that were both lightweight and visually indistinguishable from organic search results.

Walmart

One brand that found success is Walmart which figured out its pricing is more competitive than that of the whole foods market. Adhering to this value proposition and using it to attract a lot of customers. No wonder Walmart’s current revenue is 611 billion USD.

Buzzfeed

One of the brands that have nailed it is Buzzfeed, an American news and entertainment firm. They’ve gained more than 3 billion monthly content views and a global audience of more than 520 million. They focus on content sharing rather than SEO when writing.

Coco-Cola

The success of any marketing campaign is on the ability to cement the brand in the minds of consumers and one way to do this is through maintaining brand consistency. Marketing materials like websites, packaging, catalogs, brochures, letter pads, social media, print ads, TV commercials, etc. should be consistent. Use the same fonts, colors, tone, graphics, logo and images in all of those. Coca-Cola managed to maintain its brand consistency.

Amazon

Amazon’s success is credited to its customer-centric approach and its focus on innovation. Amazon’s growth strategy involves expanding its product offerings, investing in new technology and expanding into new markets. Amazon’s monitoring and evaluation system involve measuring customer satisfaction, sales growth and profitability.

Tesla

Tesla’s success is attributed to its innovative approach and its commitment to sustainability. Tesla began its journey with high-end electric sports cars then Tesla moved into the luxury electric sedan market and continued its expansion towards broader markets.

Airbnb

Airbnb’s success is due to its innovative approach and its ability to disrupt the hospitality industry. Airbnb makes money by charging both hosts and guests for using the platform, customer support and payment processing.

Conclusion

Measuring and evaluating the success of the growth strategy, analyzing the effectiveness of the growth strategy, adjusting the growth strategy and celebrating success are critical components of a successful business growth strategy. The above examples demonstrate how effective business growth strategies have contributed to their success.

We at Ruskin Felix Consulting, provide management consultancy services that also include developing successful business growth strategies for our client companies. Please feel free to contact us at contact@ruskinfelix.com.

Ruskin Felix Consulting LLC prepared a comprehensive strategy formulation report focusing on the Manuka Honey pricing analysis. The report lays emphasis on the industry characteristics, fluctuations and future scope of the industry. The report analyzes the growth drivers, industry challenges, industry opportunities and business environmental analysis. This report also highlights the financial viability of the of the project by detailing the financial assessment, costing management, absorption costing, cost allocation and pricing and revenue computation.

Manuka honey is made from the nectar of the manuka tree and is only produced in Australia and New Zealand. The key active ingredient is methylglyoxal. This is an antibacterial organic compound that can be used for both medicine and everyday health benefits. Consumer’s changing lifestyle, rising health concerns, increasing healthcare costs, and growing preference for a fit and active lifestyle are the key factors driving the demand for the it.

Manuka honey is making a comeback in the wellness world, and for legitimate reason. It is high in vitamins, nutrients, amino acids, and minerals, all of which aid in skin protection and renewal. It’s utilized in lotions, gels, perfumes, foundations, and mascara, to mention a few applications. Furthermore, it has health benefits such as strengthening the immune system, avoiding oral infections, speeding up the healing process, and stimulating the respiratory system, all of which contribute to the demand for Manuka honey. The rich flavor, as well as its expanded uses as a table sugar substitute, are driving the market forward.

The market in North America is expected to grow at the highest CAGR during the forecast period. Rapid growth in the snacking needs of children and the surge in the consumption of nutrient enriched food is fueling the growth of manuka honey market in North America. The manuka honey market was valued at US$ 741.69 million in 2019 and is projected to reach US$ 1,238.15 million by 2028; it is expected to grow at a CAGR of 5.9% from 2020 to 2028.

The growth drivers for manuka honey are as follows:

Increase in number of health-conscious individuals worldwide.

Antibacterial properties.

Therapeutic properties.

Usage in beauty products.

Rise in e-commerce contributing to manuka honey sales.

Ruskin Felix Consulting LLC created a comprehensive research and strategy report based on the Beverages industry. The reports sheds light on the overall industry analysis, market size and technical analysis which comprises of the certification analysis, calorific value analysis and sugar content analysis. The report consists of a detailed research based on the behavior and trends of consumers – behavior shifts, trend analysis, competitive analysis, and opportunity analysis. The report highlights the e-commerce strategy, B2C sales approach, and the execution plan of the project. The report lays emphasis on the business model and the brand positioning of the company.

Sales of major beverage categories are expected to grow from $150 billion to more than $160 billion by the end of 2020, according to a new report titled U.S. Beverage Market Outlook 2020: Grocery Shopping & Personal Consumption in the Coronavirus Era by Packaged Facts, a leading market research firm and division of MarketResearch.com. Most packaged beverage categories are mature, but there are still growth opportunities for companies that focus on product innovation, appeal to shifting consumer preferences, and successfully navigate market changes associated with the COVID-19 pandemic.

Over the past 2 years, the pandemic has changed the way consumers shop, socialize, entertain as well as the types of foods and beverages they consume. Although vaccines have been developed and are in distribution, the pandemic is affecting beverage trends and overall health and wellness.

From soft drinks and fruit juices to diet beverages and alcohol, the United States’ beverage market is, indeed, a profitable one. The success of the industry is illustrated by the nation’s extensive consumption of alcoholic and non-alcoholic beverages. Current estimates value the U.S. beverage market at an impressive $146 billion.

Globally, 57% of consumers report being more concerned about their immunity as a result of COVID-19. As consumers strive to enhance their immunity, they are becoming more knowledgeable about how the human microbiome supports the immune system and overall wellbeing. Products containing probiotics, prebiotics and postbiotics can benefit the microbiome and are already gaining momentum in the marketplace.

Some of the changing trend for various health sectors are as follows:

Plant based beverages is the most popular trend in the beverage industry today and has tremendous opportunity. More and more brands are coming up with plant-based alternatives as part of the product portfolio with the rise in veganism.

Juice cleanses are old school and should be replaced with beverages with low-calorie and zero calorie drinks and smoothies with popular flavors such as strawberry, mango, vanilla, chocolate etc. Tea and fruit infused beverages should also be considered while developing a new drink for the weight management ND Metabolic health segment.

With rising stress and focus on emotional well-being, this segment has tremendous opportunity. More and more people are leaning towards CBD based drinks and oils to help with their insomnia, anxiety and other illness. Some popular choices of beverages in this category are CBD infused coffee, oils, sparkling water, soda, syrup and shots.

With an increased focus on personal health and immunity after the collapse of health policies across the world due to COVID, the company should look at focusing on making immunity-based drinks focused on organically bettering the internal immune system of the consumer.

Based on the report, there are a few product recommendations that have been highlighted and emphasized on:

Probiotic beverages – To focus on Probiotics in the form of soda as it has lesser existing competition than diary-based probiotics and has a very high appeal to the millennials due to their inclination towards sugary sodas.

Wellness shots – More and more brands are focusing on ancient medicinal and apoptogenic ingredients in wellness shots and we recommend this company do the same. Ingredients like apoptogenic.

Plant-based milk – We recommend creating plant-based coffee beverages, smoothies, or desserts for this category as the milk category is already crowded with existing competition.

Weight management beverages – Low calorie and Zero sugar drinks are also another option to consider

Sports and energy drinks – The energy and sports drink market is very saturated and has many top players already existing in the market. Any new entry in the market will have to come with a huge marketing budget and celebrity endorsements to be successful.

CBD beverages – Some recommendations for products in this category would be to create CBD infused water, CBD infused soda, CBD infused coffee, and CBD infused shots.

Mocktails and cocktails – Low content alcoholic drinks in sustainable packaging like glass.

Juices – An exciting innovation being seen in North America is caffeinated fruit juice, where fruit juice is infused with cold brew coffee. This is another arm of the functional energy drink category, tapping into the demand from health-conscious consumers.

Ruskin Felix Consulting LLC prepared a report which covers an overview of the personalized gifting industry and highlights the demand for resin artwork globally and in the United States. The report analyses the various platforms and channels that can be adopted for selling resin artwork online. It explains in detail the pricing of various competitors and product segments which can be taken into consideration before setting a price for your product. The aim of the report is to provide complete strategy and analysis along with recommendations of various options that can be weighed based on cost, effort and time. Some of the key aspects covered in the report are market analysis, online aggregators, pricing strategy, traffic analysis, key competitive advantages and product placement.

Epoxy resins are a two-component system consisting of resin and hardener. By mixing the two components, a chemical reaction takes place so that the liquid resin gradually hardens to a solid plastic. The result is a high-gloss, clear surface. Epoxy Resin is a versatile material that’s used in a wide variety of crafts, including resin artwork. Resin casting is a fun way to accent your furniture, create jewelry and ornaments, etc. Resin starts as a liquid and then hardens, so you can pour it into molds, or add items like dried flowers, insects, or leaves. Because people may not have knowledge of the vast uses of resin artwork, there may be some hesitation or intimidation by the idea of trying it at home. We have provided answers to common questions we receive to help artists understand more about using resin in their upcoming art projects.

The overall resin artwork industry in the USA was valued at $170 million in 2020 and is projected to hit $331.26 million by 2027 at a CAGR of 10%. Resin artwork has been booming for a few years now, but the pandemic and lockdown all over the world have led the artists to open their own website stores and sell their art, including resin artwork, using social media. The demand for resin artwork has proliferated, and right now is a very good time to get into the industry.

The initial focus for the business should be to start with their own website for selling resin artwork products as per the niche to be focused upon. A further scaling up of units should be done through aggregators like Etsy and Amazon. The company should look at having an aggressive focus on sales and marketing through online social media platforms, including Instagram and Facebook, to promote their resin artwork.

Ruskin Felix Consulting LLC created a market research report and business plan for Al-Bidayer Holdings, UAE to understand the Cloud kitchen industry in UAE. The report consisted of an industry overview, food consumption patterns, market segmentation, total available market, serviceable available market, service obtainable market, product mix assessment, target market, qualitative analysis and assessment, geographical assessment, and location assessment. We helped in understanding the financial viability of the plan of Al-Bidayer Holdings by providing insights on the cost, revenue, and project viability assessment.

Cloud Kitchens also known as ‘dark kitchens’ is a concept with delivery only and no dine-in facility helping Al-Bidayer sell food at low costs and in a time-efficient way. They enable Al-Bidayer’s restaurants to overcome the disadvantages tied to a traditional storefront thereby reducing operational costs. Cloud kitchens are expanding rapidly in the F&B market in UAE where the food delivery sector is expected to grow at a rate of 6% annually over the next five years. The global food delivery market is expected to grow 10 times over the next 10 years and is estimated to be at $365 billion by 2030. According to the latest Redseer Consulting report, this sector is expected to have a 16% share of the total online food industry by 2023.

The global cloud kitchen market size was valued at $105 billion in 2019 and is estimated to reach $215.5 billion by 2027 with a CAGR of 12.0% from 2022 to 2027. The Total market size has also been affected by the COVID-19 pandemic; however, market demand has boosted back from earlier levels and reached much higher order levels. Cloud kitchens are also known as dark or shared kitchens. Cloud kitchens are delivery-only kitchens, which can be owned by a brand such as Al-Bidayer or third party working with various brands. Brands that are using cloud kitchens can also operate virtual restaurants or brick-and-mortar restaurants.

KaaS (Kitchen as a service): besides creating and running their brands, the model of renting out spaces or services of a kitchen for other brands to effectively come and use the spaces is a highly lucrative concept. Due to the bundle of services offered in the Kitchen as a Service model, and the advantages of the same, many brands will love to come and work with the company to deliver. This can be rented out as the whole Space (Rentals) or Kitchens Services (Profit sharing model). It is to be noted that Cloud Kitchens is more a real estate business than a food services business.

NPV for Al-Bidayer cash flows for 5 years is AED 11.29 million. This shows that Al-Bidayer is feasible and can generate high value for the company in the long run. The valuation of the company from a PE-based multiple of 10 will be about $112 million. We have also provided the Year-on Year valuation based on a cash flow-based multiple in sync with the competition valuations to assess how the valuation will increase with time.

The overall valuation for Al-Bidayer has been computed on the expected number of kitchens being opened on an annual basis. We have also accounted for an increase in the NPAT per store year-on-year. The discounting factor for computing the present value of future net cash flows is 8%. With a 5 Year forward PE Multiple of 10, the valuation of the overall business with the expected pattern of kitchen locations is AED 261.88 million.

Ruskin Felix Consulting LLC prepared a comprehensive strategy formulation report focusing on the manuka honey pricing analysis. The report lays emphasis on the industry characteristics, fluctuations and future scope of the industry. The report analyzes the growth drivers, industry challenges, industry opportunities and business environmental analysis. This report also highlights the financial viability of the of the project by detailing the financial assessment, costing management, absorption costing, cost allocation and pricing and revenue computation. We aimed to help our client create a detailed pricing strategy and policy to ascertain the prices on a national, international and quality based pricing.

The honey is made from the nectar of the manuka tree and is only produced in Australia and New Zealand. The key active ingredient is methylglyoxal. This is an antibacterial organic compound that can be used for both medicine and everyday health benefits. Consumer’s changing lifestyle, rising health concerns, increasing healthcare costs, and growing preference for a fit and active lifestyle are the key factors driving the demand for the manuka honey.

Manuka honey is making a comeback in the wellness world, and for legitimate reason. It is high in vitamins, nutrients, amino acids, and minerals, all of which aid in skin protection and renewal. It’s utilized in lotions, gels, perfumes, foundations, and mascara, to mention a few applications. Furthermore, it has health benefits such as strengthening the immune system, avoiding oral infections, speeding up the healing process, and stimulating the respiratory system, all of which contribute to the demand. The rich flavor of Manuka honey, as well as its expanded uses as a table sugar substitute, are driving the market forward.

The manuka honey market in North America is expected to grow at the highest CAGR during the forecast period. Rapid growth in the snacking needs of children and the surge in the consumption of nutrient enriched food is fueling the growth of manuka honey market in North America. The market was valued at US$ 741.69 million in 2019 and is projected to reach US$ 1,238.15 million by 2028; it is expected to grow at a CAGR of 5.9% from 2020 to 2028.

The growth drivers for manuka honey are as follows:

Increase in number of health-conscious individuals worldwide.

Antibacterial properties.

Therapeutic properties.

Usage in beauty products.

Rise in e-commerce contributing to manuka honey sales.

RFC helps clients generate long-term value for all stakeholders. We help clients transform, grow, and operate while fostering trust through assurance with our services and solutions, which are made possible by data and technology.

We balance ESG and risk mitigation in our professional services. Our consulting experts make sustainability a business priority with vision and pragmatism.

You must be logged in to post a comment.